If you’re moving or living abroad, then you need expat/international health insurance! But there’s a lot of insurance options out there, so it’s hard to know what to choose. Check out this article to learn about the best options (with pros & cons) and see tables comparing the most important features of each insurance plan.

Picture by saturnism, licensed under CC BY-SA 2.0

So you’re going to live abroad….congrats! Happy for you! ![]()

Living, working, or going to school in a foreign country can be an exciting experience. And you’ll join thousands of people just like you who have the chance to explore the world outside of their home countries. But as you make plans to get that visa and schedule that doctor’s visit for vaccinations, there’s another important thing you want to make sure you don’t forget about: expat/international health insurance.

Table of Contents

- 1 Update regarding Health Insurance for Expats and Coronavirus (COVID-19)

- 2 What is expat/international health insurance?

- 3 Why do I need international medical insurance for expats and immigrants?

- 4 Why can’t I just make sure I’m healthy before I leave?

- 5 Why can’t I just keep the health insurance I already have at home?

- 6 Can I just use travel insurance for healthcare while living abroad?

- 7 Difference between travel insurance & expat/international health insurance

- 8 What should I look for in an overseas healthcare plan for expatriates?

- 9 Who do these international health insurances work for?

- 10 Some questions to ask yourself before you buy expat/international medical insurance:

- 11 The 7 Best Companies for Expat Insurance/International Healthcare Plans

- 12 3 Bonus options for Expat International Insurance plans:

- 13 A complete table comparing these 7 health insurances for expats…

Most of you are already aware of the new coronavirus (also known as COVID-19 pandemic). And I so guess a lot of you are asking yourselves if your international health insurance covers you if you catch coronavirus.

Well, I’m not a doctor, a scientist, and I don’t work for a health insurance company. But from my research, there are usually 2 cases where you are covered by your international health insurance for expats if you contract Coronavirus:

1) You will be covered by virtually all health insurance companies and plans up to the moment you go to the hospital or doctor with flu-kind of symptoms and get your first treatment. If you’re diagnosed with coronavirus, then some health insurance policies might not cover you depending on which country you are.

2) Since the World Health Organization (WHO) has declared coronavirus (COVID-19) a pandemic, some international health insurances have exceptions in their coverage. Others follow the CDC (Center for Disease and Control) guidelines for countries with level 3 warnings.

To know more about COVID-19 pandemic coverage from the international health insurance companies mentioned below (Signa, IMG, Seven corners), please check my article Does International Health and Travel Insurance cover Coronavirus (COVID-19)?

Alternatively, you can use the links to the companies provided below and get the most accurate and updated information from their websites.

—

What is expat/international health insurance?

International health insurance for expats and immigrants covers your medical expenses while you’re living in another country long-term. Usually, it’ll cover you for a wide range of healthcare – from medical emergencies to just preventative healthcare.

As you’ll see down below, this is NOT the same as travel insurance and it’s not something you’ll want to skip.

Why do I need international medical insurance for expats and immigrants?

Just like you need health insurance at home, you also need health insurance if you plan on living in another country for more than 6 months. And many countries also require proof of medical insurance before they grant you a visa or work permit (you’ll find more about this in the “expat/international health insurance for immigration” section down below).

While you’re living abroad, you’ll still need to have regular physicals, treat any health issues when they come up, and have a plan in place in case you have a health emergency. So you will need a medical insurance that works overseas.

You may be able to get healthcare through an employer if you are being sent to another country to work, but not always. So, make sure you check with the company to find out if they have an international health plan in place for you and your family.

The good news is that you can buy an immigrant/expat insurance plan that mimics the coverage you have already at home and will give you comprehensive health coverage worldwide.

All of these international health plans I recommend below can be modified whether you are a single traveler or need family coverage.

Why can’t I just make sure I’m healthy before I leave?

Hopefully, you’ll visit your doctor before you leave your home country. But you also need to take care of yourself while you’re away. And if you have pre-existing conditions or are on maintenance medications, they won’t be covered in another country.

And as we all know…accidents happen (I broke my toe once in South Korea, I’ve met travelers who fell off their skateboard, anyone who’s spent time abroad has probably encountered food poisoning, etc.). So you want to make sure you’re covered when they do.

Why can’t I just keep the health insurance I already have at home?

Your health insurance from back home won’t cover you while you live in another country long-term. And if you aren’t a citizen of the country you will be moving to, you won’t be covered by its public healthcare system.

Can I just use travel insurance for healthcare while living abroad?

In general, no. Travel insurance is typically purchased for stays that are less than 6 months in a single country (although you can get longer plans for several countries if you’re a tourist).

Here’s a bit more info on travel insurance versus expat/international health insurance below.

Difference between travel insurance & expat/international health insurance

Travel insurance:

- Is for tourists or people who are just traveling, not living in a new country

- Usually only covers medical emergencies that happen overseas (and won’t usually cover things like basic preventative care)

- May also cover things like lost baggage and canceled flight (depending on your policy)

- Is sometimes required to travel to certain areas (like the European Schengen Area)

To learn more about travel insurance, check out our article with the 3 Best and Cheapest Travel Insurance Companies.

Expat/international/immigrant/overseas health insurance:

- Is for people moving abroad or living long-term in another country

- Works like your normal insurance from back home would

- Covers more than just emergency medical care (such as preventative care, dental, or vision)

- Can cover things like pregnancy, cancer treatment, or mental health services (depending on the plans)

- Is often a requirement to apply for visas or resident permits

- You can keep renewing it as long as you are overseas. Having international health insurance that carries over is essential for those looking to permanently relocate abroad

Expat/international health insurance for immigration and applying for residence permits/visa

In most countries, to get a temporary or permanent resident visa, you will need to prove that you are covered by some kind of international health insurance (and no, they won’t just accept travel insurance).

We all know immigration can be a bit tricky, so make sure the expat/international health insurance policy you are buying meets the immigration office requirements of the country you are moving to. You may be able to find this info online, otherwise, you’ll probably want to contact them directly.

Personal experience using expat/international health insurance for immigration in Sweden (hint: it’s not always easy):

When Nikki moved to Sweden from the United States, she needed to prove to the immigration that she was covered by an international health insurance to get her temporary residence permit. She bought a policy from one of the companies below, and it was accepted by immigration.

But then when she applied for her tax number through the Swedish tax office and needed to show proof of international health insurance again, this same policy wasn’t accepted and she had to purchase a new one with a different company.

If this is an issue you think you might run into, be sure to look into the cancellation policies of each insurance company. Then, even if immigration rejects the insurance plan you have, you won’t lose too much by canceling your current plan and buying a new one.

What should I look for in an overseas healthcare plan for expatriates?

While the plan you choose will depend on the kind of coverage you need while you live as an immigrant/expat, here are some of the basic things they should include:

- Adequate yearly benefit maximums

- Flexibility in plans and prices

- Wellness care and emergency care

- Inpatient and outpatient hospital visits

- A large network of doctors and medical facilities to choose from

- Multilingual and 24/7 customer service

We’ve compared our three favorite expat/immigration insurance options for you to check out below. All offer basic coverage for inpatient care and routine doctor’s visits, emergency evacuations, and 24/7 customer service.

Dental and vision will cost you more. If you are pregnant or plan on expanding your family while you’re in another country, you’ll have to buy the most expensive plans.

And just remember that the less expensive your plan is, the less coverage you’ll get.

So, make sure that you do your research in order to find the right plan that works for you.

Who do these international health insurances work for?

For these citizens living abroad as expats or immigrants:

- Americans

- Canadians

- Australians

- Chinese

- Germans

- French

- Argentinians

- British

- Swedes

- New Zealanders

And for citizens from almost every other country living abroad

For expats/immigrants living in:

- The United States

- Canada

- China

- Germany

- Sweden

- Spain

- Portugal

- France (European Union/Schengen Area as a whole)

- United Kingdom

- China (and Hong Kong)

- Australia

- Switzerland

And for expats living in almost any other country in the world

In other words, no matter your citizenship or which country you are moving to, most of these international health plans will work for you since they are truly global insurances.

Some questions to ask yourself before you buy expat/international medical insurance:

Do you need a private room if you’re admitted to a hospital?

Are you planning on starting a family or expanding your family?

Do you have any pre-existing conditions or are you on any medications you need to continue while living in another country?

Are you willing to pay a higher deductible for lower premiums?

Note: If you aren’t really an expat/immigrant but an international student at a school or college/university overseas, then I suggest you take a look at my article with the 3 Best and Cheapest Health Insurance for International Students and Exchanges/Study Abroad.

The 7 Best Companies for Expat Insurance/International Healthcare Plans

As always, my suggestion is that you get an online quote with all these companies I suggest. It’s a few minutes process but it can save you a lot of money when you find the cheapest option for your specific case.

1. Cigna

![]()

![]()

What I like:

- Three plans to choose from: Silver, Gold, and Platinum.

- Basic silver plan covers $100 of eye care a year and some cancer screenings

- You can modify a plan to add outpatient coverage and emergency medical evacuation if you need to leave the country to seek treatment

- They offer flexible deductibles so you can control what you pay upfront.

- 24/7 multilingual customer service

- Monthly, quarterly or yearly payment options

- Direct provider billing (Cigna pays for your appointment directly)

- Middle Eastern medical coverage

- Plans offer organ transplant services & kidney dialysis treatments

- It’s an international health insurance with good reviews

- Their website has info about your host country’s finance system, culture, and schools

What I didn’t like:

- You have to give a lot of personal information before you can get a quote.

- The basic plan doesn’t cover maternity care (so you’ll need a purchase a more expensive policy if you plan to have a baby while abroad)

2. IMG

![]()

IMG sells several kinds of insurance. From travel insurance to health insurance for students to insurance for crew members and, obviously, insurance for expatriates. So when searching on their website, look for health insurance for “Expat / Global Citizen.”

What I like:

- Have 5 plans for you to choose from

- They offer you a cash incentive and up to 50% of your deductible waived if you choose one of their facilities outside of the U.S.

- They have more than 29 years of immigrant/expat health insurance coverage experience.

- Their website features an online portal for 24/7 access and emergency medical services

- A network that includes 17,000 physicians and facilities worldwide.

- Direct billing

- They offer annual international health insurance plans as well as short-term plans

- They cover individuals & families from all nationalities

- Prices for 12-month worldwide coverage with a $250 deductible could cost less than $1000 annually for their Bronze package

What I didn’t like:

- Coverage ends at 75 years of age (but if you take out a plan before you turn 65 and keep it, you can take part in their lifetime enrollment plan)

- Basic plan doesn’t cover maternity and even their most expensive plan only covers deliveries and newborn care after you’ve been enrolled for at least 10 months

COVID-19 is considered by the company as any other illness or injury, subject to the terms and conditions of the policy.

![]()

As the name implies, Now Health International’s mission is to offer an efficient, affordable, and quickly accessible service, and nothing better than now for this.

Therefore, the focus of this company is very much on the relationship with the customer. Plan information is provided in a clear and agile manner and any possible queries are resolved by the company’s customer support team.

Now Health plans are designed to meet the daily challenges of those living abroad, providing guidance and providing quality healthcare around the world.

What I like:

- Customized plans according to your needs

- Clear information and excellent customer service team

- Provides coverage in 194 countries and territories

- Plans with high coverage routine maternity coverage

What I don’t like:

- You must wait a 12-month grace period to use maternity coverage.

- In some procedures, it is necessary to use the company’s reimbursement system, which means that you would have to pay for your care initially

German company Allianz is one of the biggest players in the world of insurance. So obviously, we can’t leave them out of the list when writing about options for international health insurance companies.

Here are a few of the things that I appreciate and didn’t like about Allianz.

What I liked:

- They have 24/7 international customer support

- Quite often, you don’t pay the healthcare provider directly (Allianz pays them directly for your treatment so you don’t need to request reimbursement)

- They offer coverage on all the continents and most countries in world

- You get access to a medical app that can help in the prevention and treatment of health problems (it’s available after 6 months of your contract and expenses up to €50 are covered)

- They have a specific program for expats or immigrants, where they help you in a number of different ways that goes beyond medical care

- Their expat insurance includes tips for health living on your own, with your family, or how to deal with a country’s specific challenges

What I didn’t like:

- Allianz don’t have many options for plans

5. Safety Wing![]()

Safety Wing is one of the largest companies for overseas health insurance, whether for students, digital nomads, and, of course, expats. Their site is easy to use and you can get a quote for their plans based on your age, length of stay, and countries covered.

What I like:

- As I said, their website is very easy-to-use and quick to get a quote

- Safety Wing covers COVID-19 for expats!

- The company is very clear about what each plan does or doesn’t cover

- It’s possible to add additional services like dentist, maternity care, deductible expenses, physical therapy & family doctor

- They offer coverage of up to $10,000 USD for repatriation after political evacuation

- You’ll receive payment help if you’re treated in a public hospital without fees or when the treatment is covered by another insurance (in these cases, you’ll receive US $125 per night for up to 30 nights)

- They have full coverage and reimbursement for cancer treatments and reconstructive surgeries

- They cover insurance for children under 10 without any additional costs

- You can get 24/7 customer support anywhere in the world

- They also cover visits to your home country for 30 days every 90 days

What I didn’t like:

- The coverage for United States, Hong Kong, and Singapore has quite high fees

- You need to create a login and fill out a lot of information before getting a quote

- Quotes don’t show all fees

Safety Wing also covers COVID-19 in their expat insurance plans. And as of August 1st, 2020, this coverage is available for their nomad plans.

However, COVID-19 tests are only covered when they are deemed necessary by a doctor. Antibody tests, on the other hand, are never covered as they are not medically necessary.

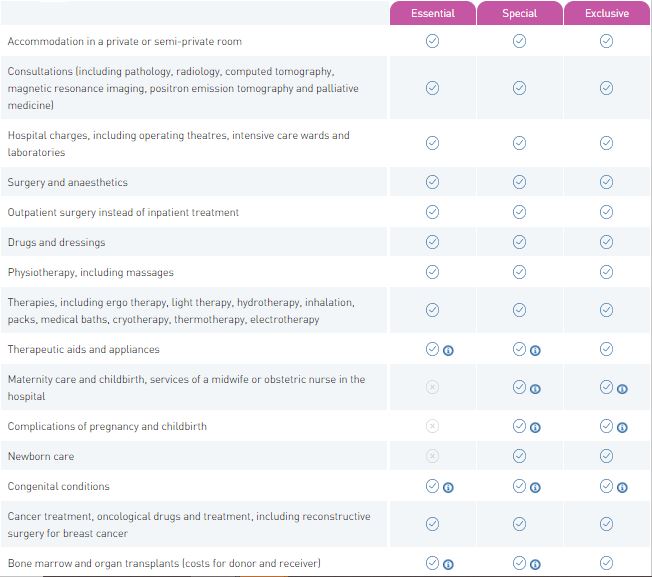

Part of the Foyer Group, a huge European enterprise, Global Health is specialized in many types of insurance – from travel insurance to expat and student insurance. Beyond being a reliable and well-known company, it may also have the largest variety of personalized plans for you to choose from.

What I like:

- It’s possible to personalize your insurance coverage based on your age, country of origin, dental care, eye care, maternity & small child care, and more (you can even choose the amount of coverage you want from

- It’s possible to choose insurance for a single person, for a family without children, or for a family with children

- Even if you don’t have U.S. health insurance, you’ll be covered with emergencies while on American soil

- Beyond the personalization above, you can also choose between ESSENTIAl, SPECIAL, and EXCLUSIVE

- It’s very easy and quick to get a quote – minimal personal information needed

- There are options for deductibles

- It’s possible to get short-term plans if you don’t plan to stay long in another country

- It’s possible to do a comparison between the plans to decide which is right for you

- They offer health coverage options for expats all over Europe

What I didn’t like:

- The coverage for the most simple and basic plans leaves out many things like maternity care and newborn care

- The customer service, although it seems to work fine, isn’t as straightforward as the others on this list

- The website isn’t so clear about what is/isn’t covered and the limits

- The website gives a lot of info about coronavirus, but it isn’t clear if any of their plans do/don’t cover tests of COVID-19 complications

- They charge a 5 euro fee for emergency support

Another good insurance option for expatriates and immigrants is Global Underwriters, they have been in the market for years offering differentiated plans for travelers from all over the world.

The best plans for expatriates are Diplomat Long Term and Diplomat International, both of which serve the needs of residents in foreign countries very well and have very complete coverage.

What I like:

- Plans cover medical evacuations, repatriation of remains and emergency dentistry

- They have coverage of up to $1,000,000 for medical care and accidental death or dismemberment

- They offer assistance in case of interruptions during the trip caused by health problems and assistance in case of lost luggage

What I didn’t like:

- The Diplomat Long Term plan does not serve citizens residing in New York, Maryland, South Dakota, as well as residents of Australia and Iran

- The Diplomat Long Term plan does not cover travel to Cuba, Iran and Afghanistan

- The Diplomat International plan does not cover care for Covid-19

3 Bonus options for Expat International Insurance plans:

– GeoBlue![]()

GeoBlue is an excellent choice of insurance for expatriates, and if you are a resident of or visitor to the United States it is the perfect choice. This company meets the highest quality standards and is among the leaders in its category.

What I like:

- Service that meets the highest quality standards

- Flexible plan designed especially for expatriates and foreign nationals living in the US or US citizens living in

- With the Xplorer plan, you have no deductible for standard services and an unlimited medical cap

- The Xplorer plan covers extreme sports and has no cancellation fees

- Optional dental and vision options

- Several plans to choose from

- 24 hour service 7 days a week

- Plans with full coverage, from evacuation, health consultations to maternity care

What I didn’t like:

- Not available to residents of New York and Washington

- For pricing, you must contact a broker

GeoBlue offers unlimited telemedicine consultations completely free of charge for members of its plans with Covid-19 questions. If requested by a physician, the company also covers clinical testing and treatment for Covid-19

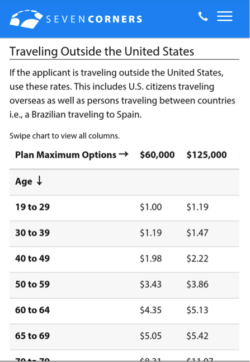

– Seven Corners Liaison Majestic

As with IMG, Seven Corners also has medical insurance for travelers, students, faculty, and others.

What I like:

- They have a 20-year history providing international health insurance options

- Offer plans that cover pre-existing conditions

- They’ll locate an embassy for you and give you travel advisories

- 24/7 multilingual travel assistance

- Their plans offer inpatient, outpatient, dental, emergency evacuation and emergency reunion (a friend or family member to be flown to be at your side while you are in the hospital)

- You can add a hazardous sports rider that covers hang gliding, zip-lining, water skiing, and bungee jumping.

- Basic plans are reasonably-priced – A single male moving to Fiji can get a basic plan with a $250 deductible for about $1 a day

What I don’t like:

- You can’t get a plan if your U.S. address is in Maryland, Washington, New York, South Dakota or Colorado

- Can’t get coverage if you’re above 60 years old

- They don’t provide coverage in if you’re going to Iran, Syria, U.S. Virgin Islands, Gambia, Ghana, Nigeria, or Sierra Leone

- You need to have precertification for certain services like inpatient stays, rehab, and outpatient surgeries, and home healthcare

– Aetna (acquired by Allianz)![]()

Aetna is a company that makes it a priority to provide its customers with services that are in line with their actual needs. For this reason, this company works with a variety of plans tailored to expatriates and citizens living in various countries around the world.

What I like:

- It is a solid company that has been in business for over 50 years

- They set up tailor-made plans for expats and digital nomads

24 hours a day, 7 days a week service - Most plans offered include full coverage for hospitalization, emergency evacuation, repatriation and cancer treatment

- Has won awards for “Best International Private Health Insurance Provider” and “Health Insurer of the Year

- Aetna has developed an application where you can monitor your health, and by practicing healthy habits users earn points that can be redeemed for gift cards at popular stores

- Covers expatriates and foreign residents in more than 15 countries and territories worldwide

What I didn’t like:

- They do not offer travel insurance plans for solo travelers or families

- Website could be more clear and intuitive when presenting available plans

Aetna International fully covers the cost of Covid-19 treatment and testing for members of some of its plans, such as Medicare. To find out which plans are covered, you need to contact the company.

Do you consider yourself a “global citizen,” or are you a digital nomad and need medical insurance that will follow you worldwide?

If so, the insurance above works for you too. The 7 international health insurances listed are ideal for digital nomads or any person who keeps living all over the world and doesn’t have a fixed country of residency. After all, “global citizens” deserve global health insurance! ![]()

Quick summary comparison of the 7 international health insurance plans:

| CIGNA | IMGLOBAL | AETNA | GEOBLUE | SAFETY WING | GLOBAL HEALTH FOYER | GLOBAL UNDERWRITERS |

| Silver – $1 million | BRONZE – $1 million | The values of the limits increase depending on the length of the insurance contract | The coverage amounts may change according to your choices | Annual benefit maximum of US $1,000,000 | Personalized plans for you or your family | Maximum annual benefit of $1,000,000.00 |

| Gold – $2 million | SILVER – $5 million | Aetna’s plans may cover cancer treatments when the patient is part of a clinical trial. | Full reimbursement for hospital & cancers treatments, ambulance, and reconstructive surgeries | Value of total coverage is something you can customize per item | Up to $1,000,000 coverage in cases of accidental death or dismemberment | |

| Platinum – Unlimited | GOLD – FOR COVERAGE UP TO 36 MONTHS – $5 million | Value of total coverage is something you can customize per item | ||||

| GOLD – FOR COVERAGE AFTER 36 MONTHS – $5 million | ||||||

| GOLD PLUS – $5 million | ||||||

| PLATINUM – $8 million |

A complete table comparing these 7 health insurances for expats…

|

|

|

|||||

| BENEFIT | LIMIT | LIMIT | LIMIT | LIMIT | LIMIT | LIMIT | LIMIT |

| Benefit Information | |||||||

| Medical Maximum | Unlimited (for the Platinum plan) | $8,000,000 | The site doesn’t specify | Unlimited | US$1,000,000 per year | The site doesn’t specify | $1,000,000 |

| U.S. In-Network Coinsurance | You choose. From 70%(100% thereafter) to 100% | 100% | No | 60% for maximum coinsurance and then 100% | Yes, for higher fees | Only in emergencies | Yes |

| U.S. Out-of-Network Coinsurance | You choose. From 70%(100% thereafter) to 100% | 90% to $5,000 (100% thereafter) | Yes, for higher fees | 100% | 100% | 100% | 100% |

| Mental Health Availability | No waiting period | 12-month waiting period | Co-payment of $25 per visit, waived deductible | 75% up to 40 visits / 60% after that | No | Waiting period of 10 months | Depends on the plan |

| Mental Health Benefit | Inpatient and Outpatient: $5,000 lifetime maximum to paid in full depending on the plan | Inpatient and Outpatient: $50,000 lifetime maximum | Co-payment of $250 after deductible | 100% up to 60 days | International and ambulance: limit not specified | ||

| Inpatient Prescription Drugs | $500 to paid in full depending on the plan | Up to $8,000,000 | Yes | Complete reimbursement | Yes | Yes | |

| Outpatient Prescription Drugs | None, unless you buy the International Outpatient Option | Up to $8,000,000 | Complete reimbursement | Yes | Yes | ||

| Evacuation and Repatriation of Remains | Paid in full | Up to $8,000,000 | Yes | Up to $25,000 | No | Up to 10,000 euros | Yes |

| Accidental Death & Dismemberment | Depends on the plan | Rider available, limit depends on age. | $50,000 | Depends on the plan | |||

| Emergency Dental | Paid in full | Up to $8,000,000 | Optional | 1,000 per year, $ 200 per tooth | Yes, however you need to pay an extra fee on top of your plan | Depending on the plan, it’s unlimited | It has coverage in the Diplomat Long Term and Diplomat International plans |

| Treatment Necessary as Result of Terrorism | Up to the amount of the coverage | Rider available up to $50,000-lifetime maximum | Clause available up to maximum of $50,000 in lifetime payments | ||||

| Amateur Sports | Unlimited | Rider available up to $10,000 | No | Yes | No | No | No |

| Newborn Care | |||||||

| Routine Nursery Care of a Newborn Child of a Covered Pregnancy | $25,000 to $156,000 depending on the plan | $1,000 additional deductible, $50,000 lifetime maximum, $200 wellness benefit for first 12 months | Yes | Depends on the plan | Can be unlimited depending on the plan | Can be unlimited depending on the plan | |

| Children born as a result of fertility treatment (such as IVF or surrogacy) | Only after the baby is 90 days old | Excluded | Depends on the plan | Excluded | No | ||

| Neonatal Intensive Care Unit | Check website for updated information | $250,000 maximum for first 31 days | No | Up to $250,000 for the first 31 days | No | ||

| Pre-existing Conditions | |||||||

| Pre-existing condition exclusion period | Conditions that are fully disclosed on the application and have not been excluded or restricted by a rider will be covered as any illness | Conditions that are fully disclosed on the application and have not been excluded or restricted by a rider will be covered as any illness | Conditions that are fully disclosed on the application and have not been excluded or restricted by a rider will be covered as any illness | Conditions that are fully disclosed on the application and have not been excluded or restricted by a rider will be covered as any illness | Conditions that are fully disclosed on the application and have not been excluded or restricted by a rider will be covered as any illness | Conditions that are fully disclosed on the application and have not been excluded or restricted by a rider will be covered as any illness | Conditions that are fully disclosed on the application and have not been excluded or restricted by a rider will be covered as any illness |

| Pre-existing condition look back period | Any time prior to effective date | Any time prior to effective date | Any time prior to effective date | Any time prior to effective date | Any time prior to the effective date | Any time prior to the effective date | Any time prior to the effective date |

| Pre-existing annual maximum once covered | Unlimited depending on the plan | Up to $8,000,000 | Unlimited depending on the plan | Unlimited depending on the plan | Full reimbursement | Unlimited depending on the plan | Unlimited depending on the plan |

| Pre-existing lifetime maximum once covered | Unlimited depending on the plan | Up to $8,000,000 | Unlimited depending on the plan | Unlimited depending on the plan | Full reimbursement | Unlimited depending on the plan | Unlimited depending on the plan |

Worldwide Medical Insurance / Comparison Chart*

Part of the table courtesy of Tokio Marine HCC

*Note: this table is just for informational purposes and subject to change. It was accurate as of the time we wrote it here, but please check each company’s individual website for updated info.

To sum up…

These are the 7 best international health insurance for expats and immigrants:

- Cigna

- IMG

- Now Health

- Allianz

- Safety Wing

- Foyer Global Health

- Global Underwriters

In conclusion…

The bottom line is if you are going to live in another country temporarily or permanently, you need to get yourself an immigrant/expat health insurance plan.

But we know it can be a little bit overwhelming to choose the right plan. We’ve been through this personally so please, leave a comment below if you have any questions or if there’s anything you think we’ve missed!

Do you live abroad and need to receive or send money back home cheaply?

I have a specific article to help you make international transfers as cheaply as possible: The 5 Best Websites for International Money Transfers (send and receive money from abroad).